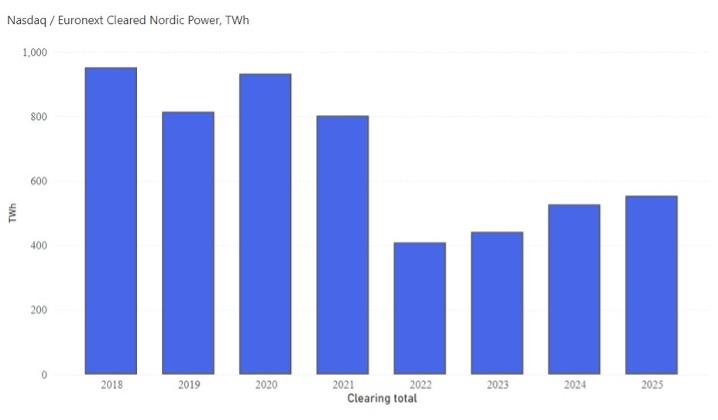

A significant share of Nordic electricity derivatives trading already occurs bilaterally. In recent years, exchange-traded volume has fallen by about one-third, while bilateral trade volume has nearly doubled.

“The reasons for this shift include the energy crisis, daily cash settlement of futures, tighter regulation, limited supply from Nordic clearing banks, and long-term renewable energy PPAs. The question is why only a few players have benefited from a changing market, and how market participants can turn the situation to their advantage,” says Suvi Paaso, CEO of Power-Deriva.

Power-Deriva’s CEO, Suvi Paaso, is shaping the future of electricity derivatives trading.

PD Port: Your platform for fair and easy bilateral electricity derivatives trading

According to a Fingrid study, bilateral electricity derivatives trading is largely conducted by large and state-owned entities. As a result, smaller operators have had no visibility of actual price levels and have been unable to benchmark prices effectively. Finding counterparties has also been a challenge.

PD Port changes the dynamic: PD Port is a marketplace for bilateral electricity derivatives, where market participants can view open bids and market interest in a single view. Trading is possible between counterparties under an existing framework agreement.

“PD Port is set to transform bilateral derivatives trading. We are increasing transparency and helping market participants manage contracts and counterparty risk. By mid-May 2026, PD Port had secured 11 letters of intent, and change is underway,” says Paaso.

The transformation of electricity derivatives trading, 2018–2025.

What the forerunners in electricity derivatives trading have to say

Turku Energia‘s interest in PD Port was sparked by persistently weak liquidity in electricity derivatives trading based on regional price differences. Hedging against regional price spreads is particularly challenging because the number of market participants in each area is typically small. Finland currently has just one price area, which helps, but Sweden and Norway, for instance, have several. Turku Energia is also concerned about the broader decline in liquidity in derivatives trading. Time will tell whether the shift in liquidity in the electricity derivatives market is permanent.

“Transparency is a prerequisite for a competitive market. Everyone benefits from effective price hedging, consumers included. It’s great to be involved in developing PD Port through an active forum, and to have our views genuinely heard,” says Ari Lahti, Portfolio Manager at Turku Energia.

For Oomi, hedging is at the core of its business, with fixed-price electricity contracts hedged using derivatives. The company, which serves more than 800,000 residential and business customers, has been a Power-Deriva partner for years.

“Power-Deriva has built the platform with real thought behind it. They actively seek our input and develop the service alongside us. We’re excited to play a part in shaping PD Port’s development. I believe the new marketplace will make a portfolio manager’s day-to-day work significantly easier,” says Antti Tammi, Trading & Portfolio Development Lead at Oomi.

Alongside numerous sales and generation companies, a major Nordic energy-sector integrator is also working to advance transparent and efficient trading in bilateral electricity derivatives.

“This particular player’s annual trading volume amounts to tens of terawatt-hours,” Paaso notes.

Why now is the right time to join PD Port

Players who come on board early will have the opportunity to shape the platform’s development through the Customer Advisory Board, to establish framework agreements, and to secure a position one step ahead of the rest.

“PD Port is a shared opportunity for the entire energy market. The snowball has started rolling,” says Paaso.

Joining the PD Port marketplace begins with a letter of intent, after which participants can expand their counterparty network and stay up to date with PD Port’s developments via a newsletter. Power-Deriva can support parties with contract negotiations and, once PD Port is operational, provide counterparty risk management as a separate service. The product range covers baseload, EPAD, SYS, and combo products, with a minimum of 0.1 MW, available on monthly, quarterly, and annual terms across the Nordics and the Baltics. Membership fees start at €250 per month, with a volume fee starting from €0.015/MWh.

“There’s also a financial incentive for the fastest movers: a membership agreement signed by 1 November 2026 entitles the signatory to a 35% discount for the first six months after PD Port launches,” Paaso promises.

Join PD Port by 1 November 2026 to get 35% off your first six months.

Book a meeting or get in touch.

Let’s map out your opportunities: